[ad_1]

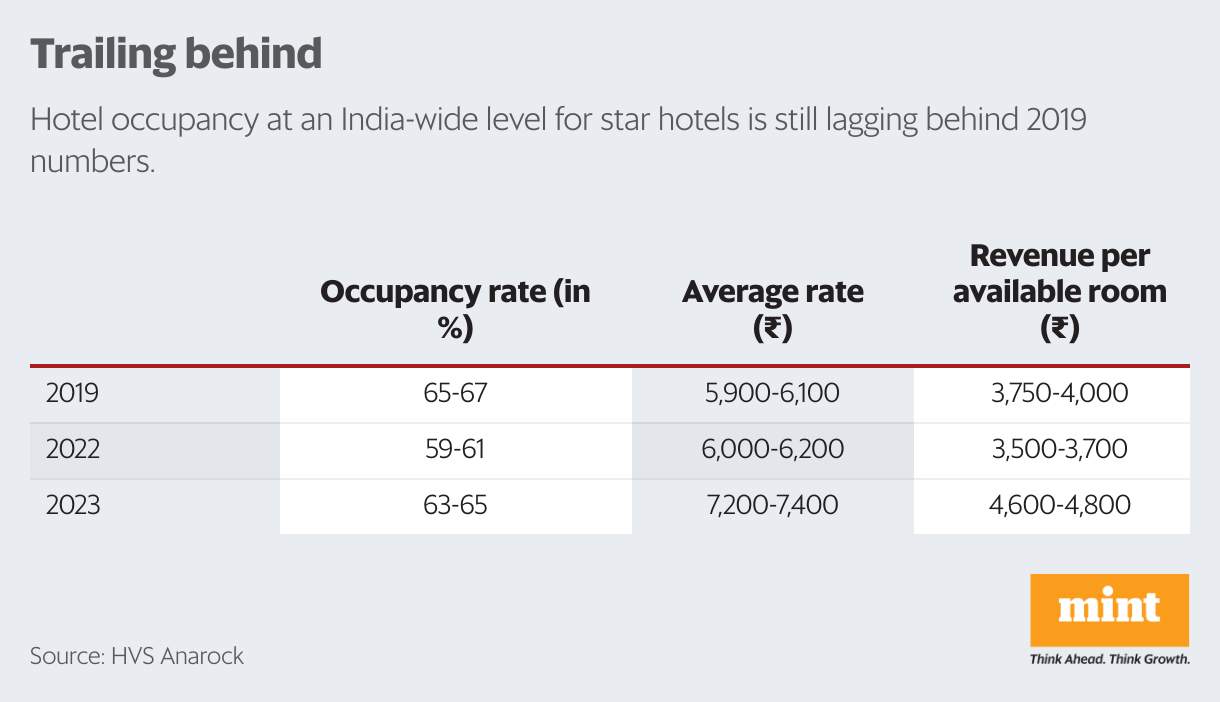

The organized hotel industry— which has about 200,000 branded rooms across the country—is expecting to end the year with an occupancy rate of 63-65%, marking a five-percentage-point increase from 2022, but still 1-2 percentage points below 2019. But because most hotels charged far more money than they did in 2022 and 2019, the revenue gap did not show.

Room rates have been a pain point for most customers. According to data put together by two top hospitality consultancies exclusively for Mint, the average room rates are far higher than their range in 2019.

On an average this year, the traveller had to shell out ₹7,200-7,400 for a room in the top hotel brands, indicating a year-on-year increase of 20%, and 22% higher from 2019, said data from HVS Anarock.

This upward trajectory has also resulted in a 30% increase in Revenue Per Available Room (RevPAR) from ₹4,600-4,800 in 2022, and a 20% uptick from 2019 levels. RevPar is calculated by multiplying a hotel’s average daily room rate (ADR) by its occupancy rate.

Mandeep S. Lamba, president, South Asia, HVS Anarock, said that travel demand reached an all-time high, and hotel companies are strategically expanding their portfolios to meet this escalating demand, especially focusing on tier II and III cities.

JLL India, on the other hand, which compiled the transaction volumes in the sector, said the total transaction volume is still a third of 2019 levels.

It said that hotel transactions— hotels bought and sold—totalled ₹5,850 crore in calendar year 2019, but only ₹2,050 crore worth of transactions have happened between January and November 2023.

The company has taken into consideration greenfield, brownfield and conversion/rebranding projects. On an average, greenfield hotels take 4-5 years to complete and become operational. Brownfield and conversions take much less time.

Hotel occupancy at an India-wide level for star hotels was still lagging behind 2019 numbers by 2.9% and showing just a 3.4% growth in the 11 months, over 2022 figures.

In 2022, about 9,900 keys or rooms were added to the organized hotel supply, while between January and November 2023, over 12,400 rooms across the country have already been added, a 25% growth compared to calendar year 2022. Of this, 60% of the total openings are from tier-III destinations, and 34% from tier-II cities.

“In the medium term, it is expected that India’s demand for hotel rooms will surpass the available supply. While tier-I markets have reached maturity, tier-II and III cities are swiftly and steadily harnessing their demand potential,” said Jaideep Dang, managing director of hotels & hospitality group at JLL India.

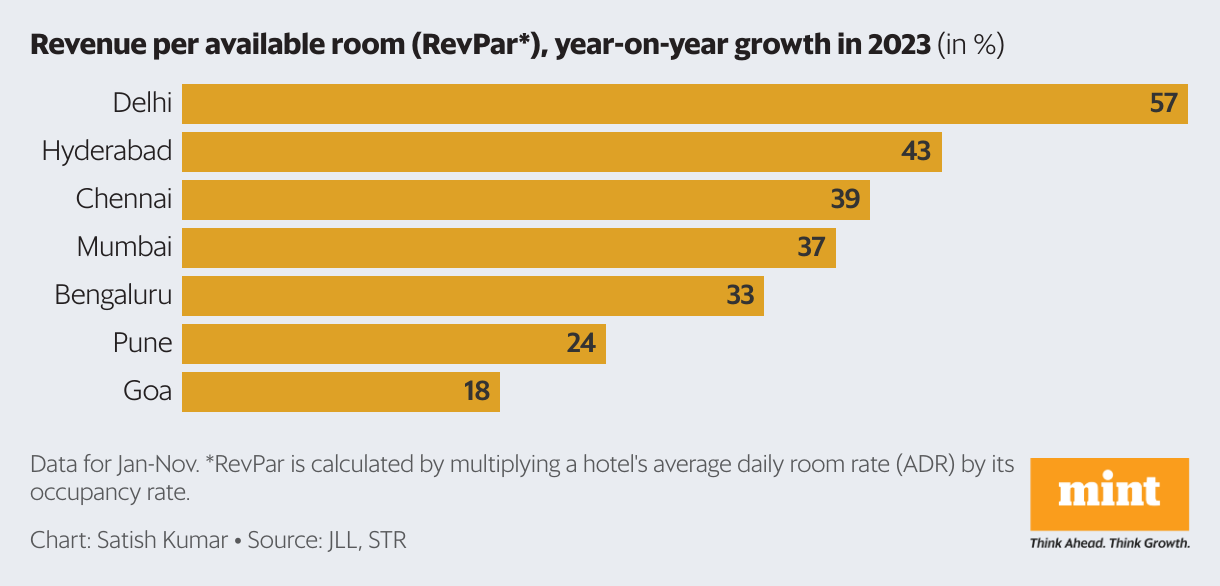

In terms of cities that performed well, Delhi had the best revenue per available room performance in the 11 months of the year, versus the same period in 2022. The city outdid itself by 57% because of return of business in the form of MICE (meetings, incentives, conferences, exhibitions) events, as well as in-bound and corporate travel. Following the capital was Hyderabad at 43% RevPAR. Bengaluru, Mumbai, and Chennai hovered well above the 2022 range, registering an increase of RevPAR between 33% and 39%. Demand in these cities is largely driven by domestic travellers from the corporate sector.

Goa saw the lowest change in this metric at 18%, but this could be attributed to the fact that the state was already trading at very high room night costs last year as well. JLL said it facilitated deals worth ₹1,000 crore in India in the calendar year, covering 900 hotel rooms.

Until November 2023, the total investment volume in the Indian hospitality sector has grown by over 250%, with an approximate investment of ₹2,050 crore, compared to just ₹580 crore in 2022.

While the last two years witnessed a variety of transactions such as single asset sales, consolidations, and lease agreements for greenfield airport hotels, 2023 also saw an increase in investment activity resulting from NCLT (National Company Law Tribunal) proceedings, especially involving high-value assets burdened with debt in strong performing markets such as Mumbai and Bengaluru.

While greenfield developments have made a strong comeback, the hotel investor sentiment continues to have a preference for high-quality assets that are already operational in established as well as key emerging markets.

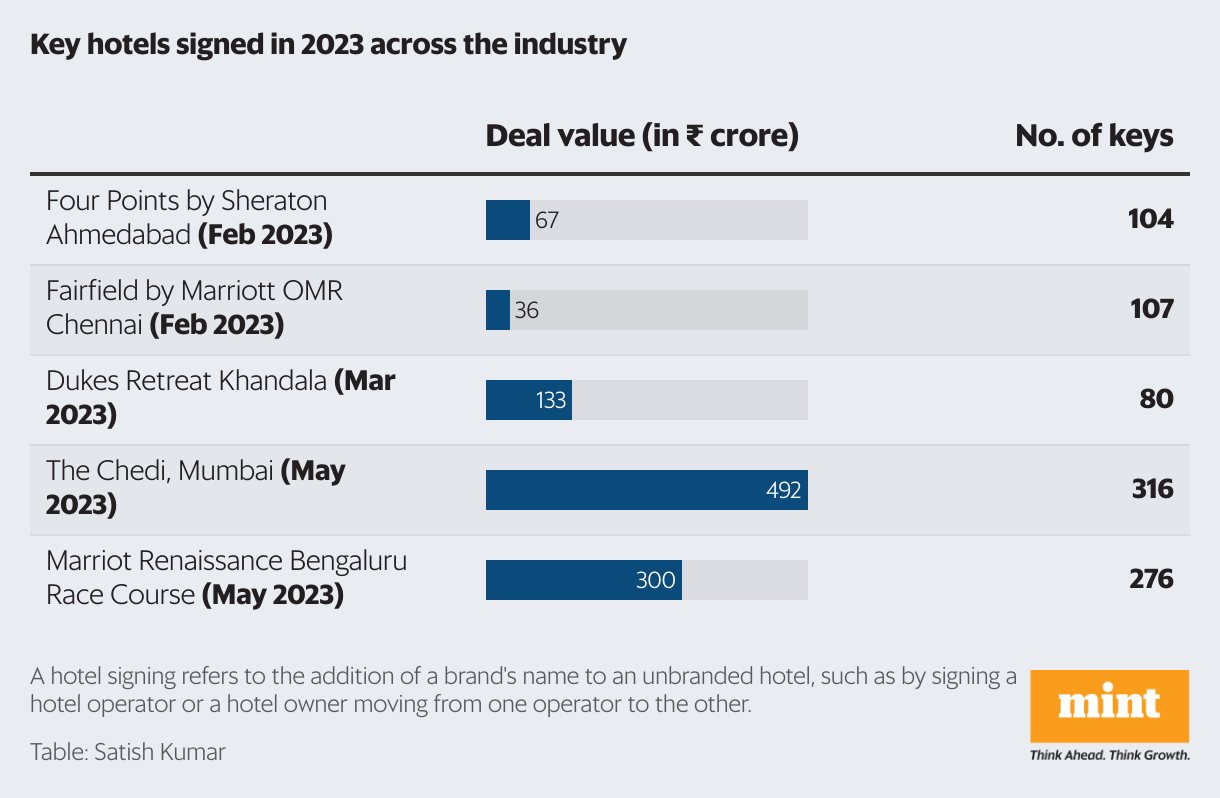

For the first three quarters of the calendar year 2023, data has recorded the signing of 16,300 keys across various segments, with 45% of the signings in the midscale hotel category.

Over 55% of the total signings have been recorded in tier III destinations, where management contracts have emerged as the preferred engagement format followed by franchises.

[ad_2]

Source link