[ad_1]

Every month, Mint’s Plain Facts section brings out an update on key global economic data to thread together the biggest developments in the world that are worth paying attention to. The accompanying analysis and charts attempt to explain how each story is creating ripples on the global stage, where it is headed in the coming weeks, and whether it can impact India. This month, we explain how economies are falling prey to recessions, Türkiye’s never-ending troubles with inflation, and rising global temperatures.

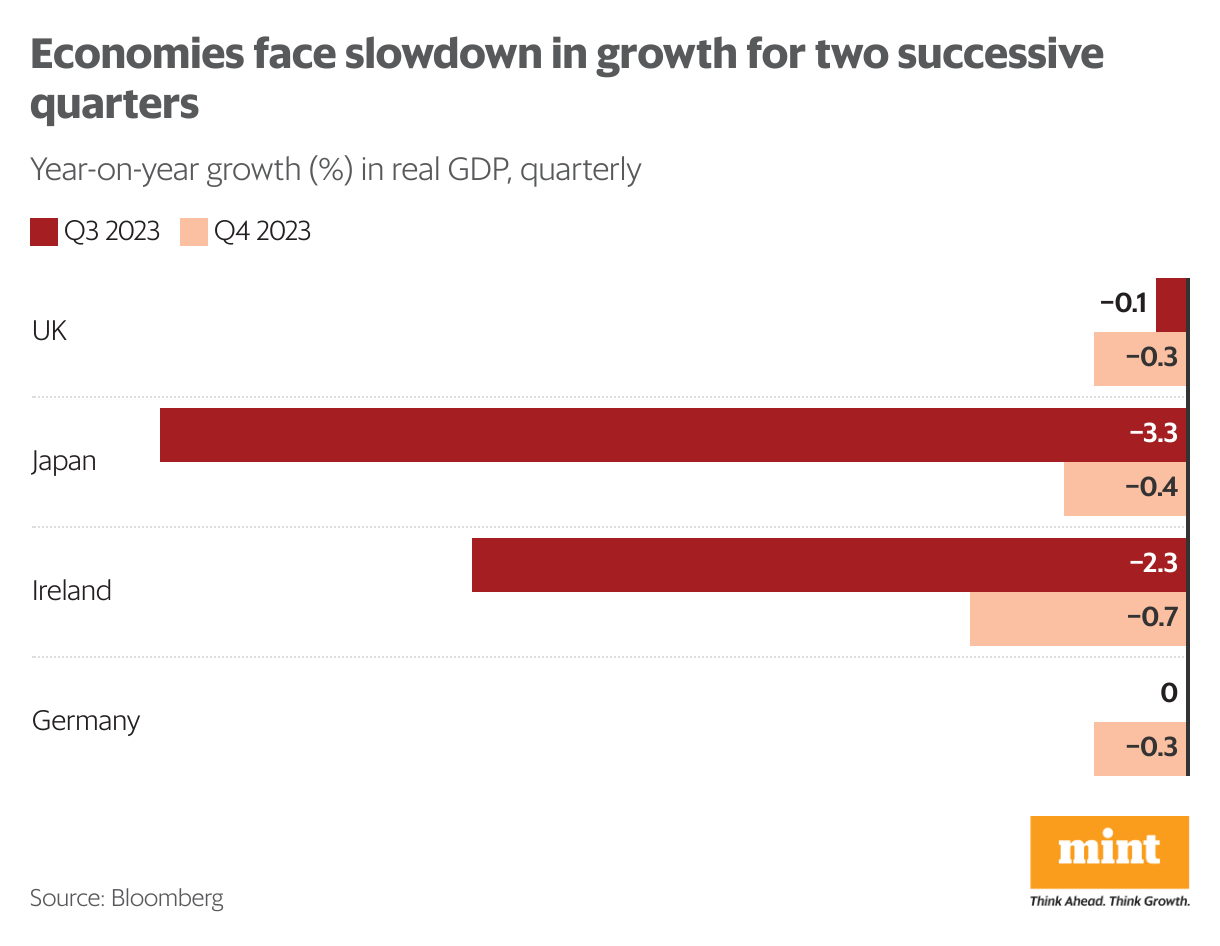

1. Slowdown blues

Two G7 economies slipped into a technical recession (two successive quarters of decline in GDP growth) in the December-ended quarter. With a 3.3% decline on top of a 0.4% contraction in the September quarter, Japan has now lost its title of the world’s third-biggest economy to Germany. The decline has reportedly been due to a fall in the value of the yen, which slumped over 18% against the dollar in 2022 and 2023. The UK also reported negative economic growth in both quarters of the second half of 2023—first 0.1%, and then 0.3%. However, the relatively modest magnitude of these contractions suggests that the UK might be experiencing stagflation rather than a full-fledged recession at this point. The downturn is not limited to these two economies alone. Israel, Finland, Germany, and Ireland also shrank in the December quarter. For Ireland, it was the fifth straight quarter of slowdown.

2. War-hit economy

Israel’s all-out war in Gaza since 7 October last year has taken a heavy toll on its economy. The country’s GDP plunged a whopping 19.4% in the December quarter. This is the first estimate since the war began. In the same quarter last fiscal, the country’s economic growth had expanded by 6.4%. Private spending has shrunk and so have investments in fixed assets. Sequentially, private consumption saw an annualized decline of 26.9%, while fixed investments dropped by almost 68%. Reports suggest that the war has also led to shortage of labour as Israel has mobilized 300,000 men and women as military reservists. Besides, many Palestinian workers from the occupied West Bank, who earlier used to cross borders to work in Israel, have been barred from doing so since the war began. As a result, many sectors, specifically construction and agriculture, have been affected. However, government spending has surged due to war-related expenses, compensations for victims’ families, and evacuation measures.

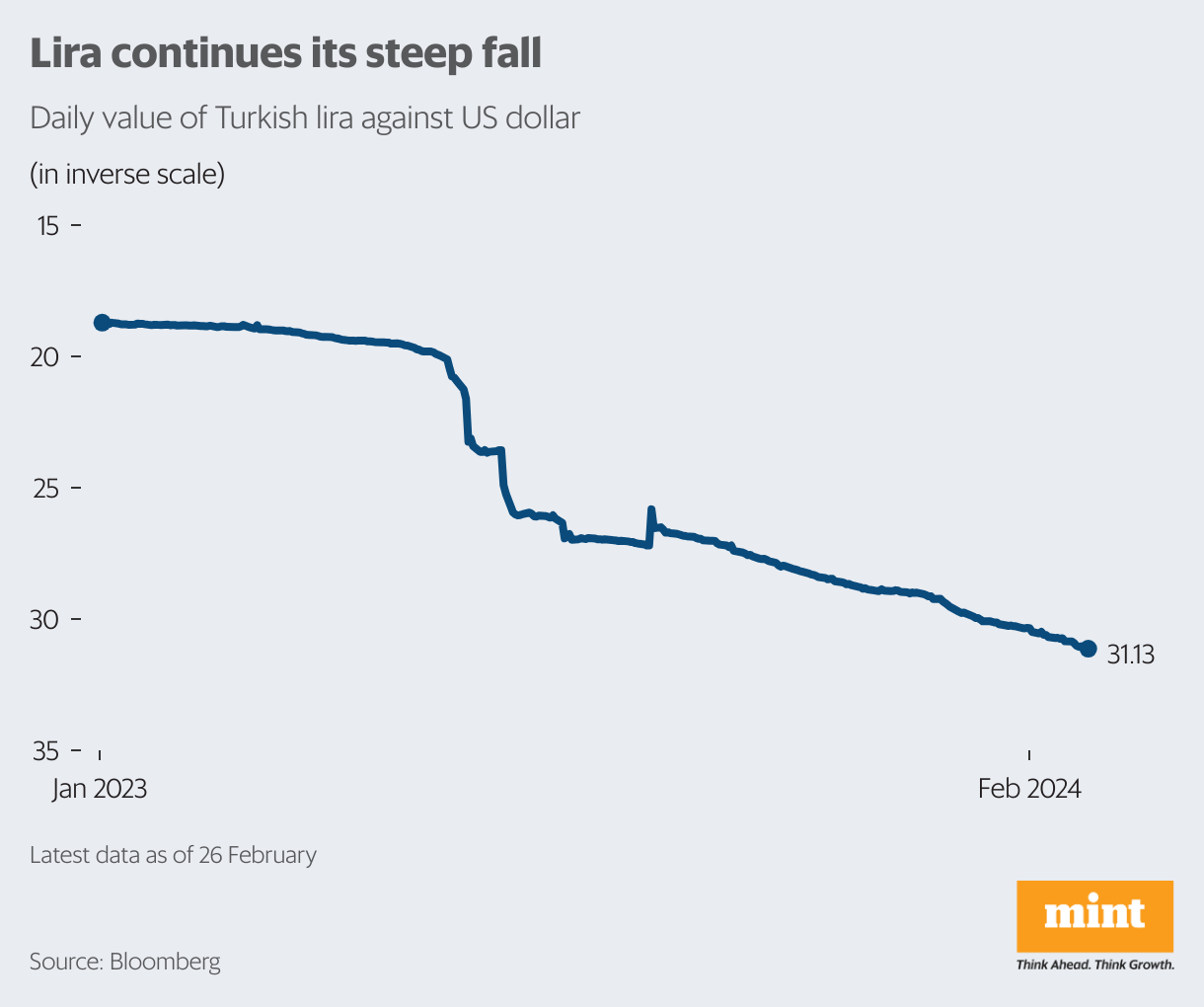

3. Turkish gloom

The Turkish economy has been reeling under the pressure of rapidly rising prices for quite some time now. In January, inflation reached almost 65% year-on-year, the highest since November 2022. The month-on-month jump of 6.7% in prices was the biggest since August 2023. Reports suggest that the 49% rise in minimum wages announced by the government in December as an aid for people to deal with the rising cost of living has inflamed inflation further. The move was made ahead of the March 2024 local elections. The ‘hotels, cafes and restaurants’ sector experienced the biggest annual rise in prices (92.3%), followed by education (79.8%) and health (78.6%). In a bid to bring down inflation, the central bank has announced eight back-to-back interest rate hikes since May 2023. The lira has also been under stress as it plunged to an all-time low against the US dollar on 21 February.

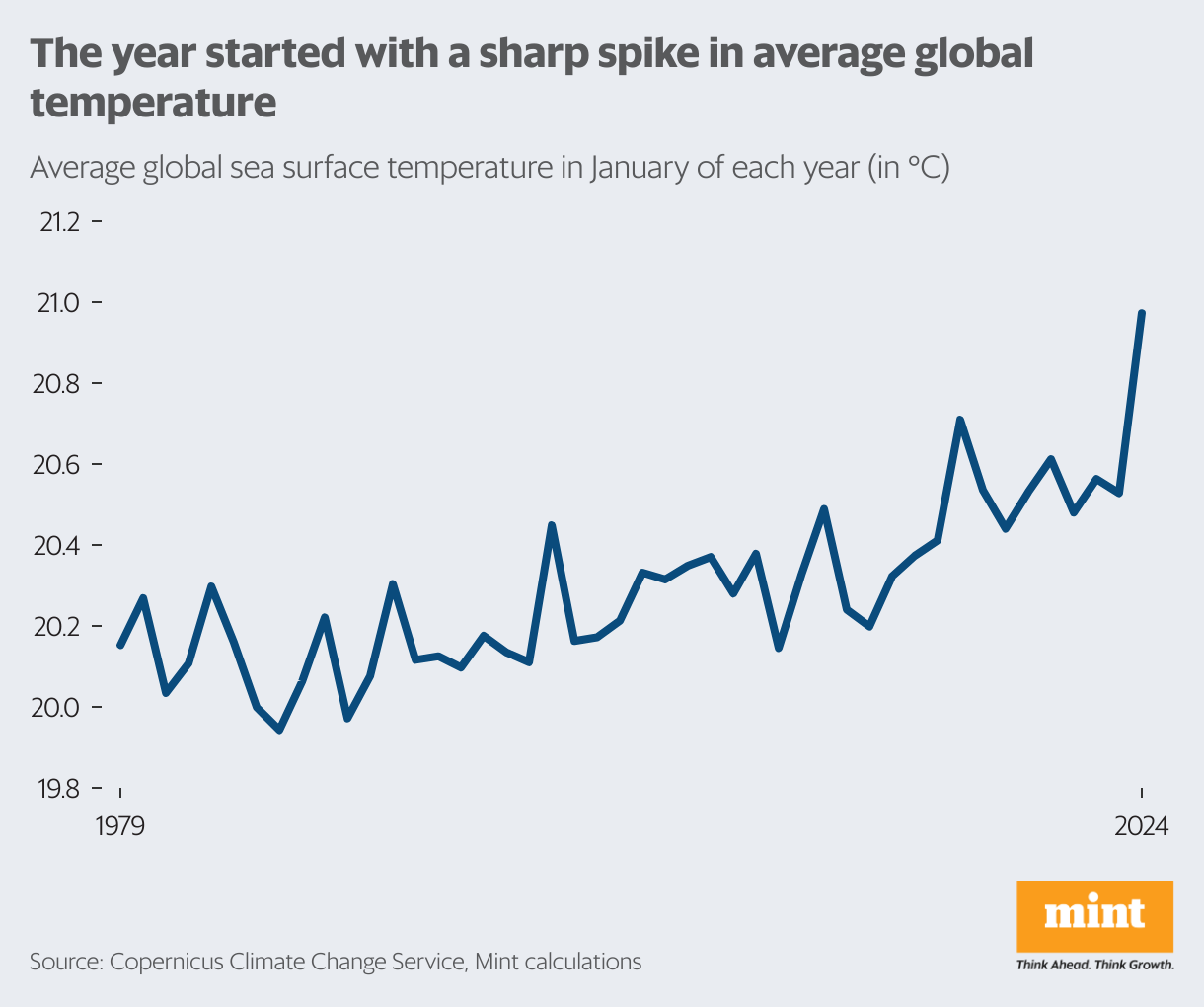

4. Global ‘warning’

Last month, the world recorded the warmest January at least since 1940, and the 12-month global average temperature (February 2023 to January 2024) rose past the critical 1.5°C mark relative to the pre-industrial period, the European Union’s Copernicus Climate Change Service (C3S) said. The rise in temperature along with climate change is already causing problems for several countries, with the agriculture economy taking a hit. Over a decade ago, climate scientists had chosen 1.5°C as the threshold beyond which certain effects of climate change would become irreversible. It refers to the difference between the average global surface temperature as compared to the pre-industrial climate of the late 1800s. In 2015, world leaders from 195 countries had signed the landmark Paris climate agreement, pledging to limit temperature rise within this threshold. However, in November 2023, a United Nations report had said that there was a vast gap between actions planned and what needed to be done.

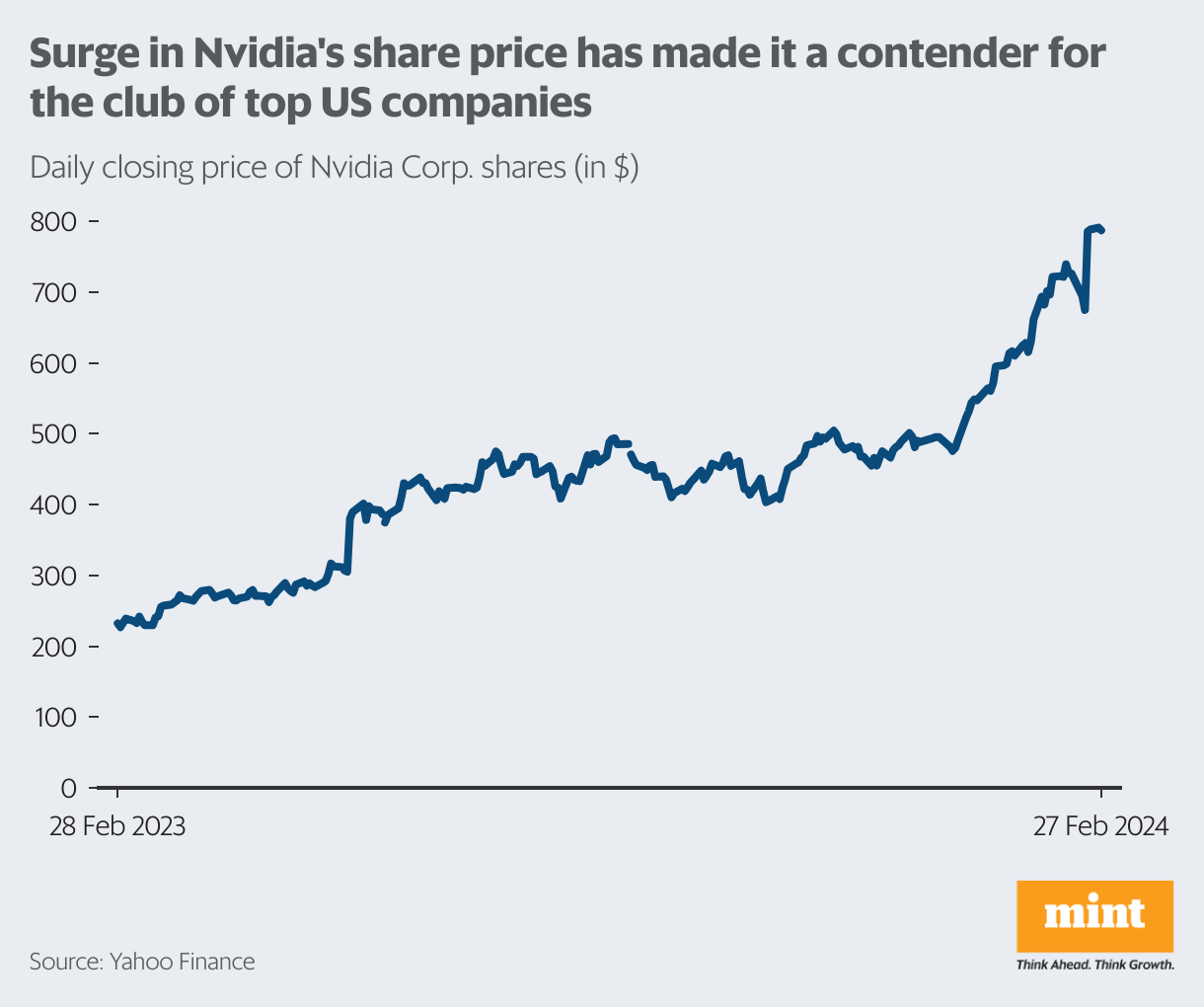

5. Roaring Rally

The breathless rally in the share prices of Nvidia Corporation, a chip-maker based in the US, has made it a contender to join the club of the world’s biggest companies. In February, it surpassed the $2-trillion mark in market capitalization, albeit briefly, after a strong revenue forecast. Nvidia’s stock has gained nearly 60% in 2024 so far. The company, which is a leading supplier of chips in the artificial intelligence (AI) revolution, has already surpassed Amazon and Alphabet in market value. With the rise in adoption of AI by several companies, the company has seen a massive interest and is set to benefit from the technological shift. The roaring rally by Nvidia wasn’t only good news for the US, but the spillover effect also lifted Asian tech stocks. As a result, Japan’s Nikkei 225 surpassed its previous record set in 1989 last week. The surge in Nvidia’s shares has brought in optimism amid recession bells ringing in Europe.

[ad_2]

Source link